Global bonds play an important role in your portfolios, providing a defensive return element (which has been tested in recent years) and ongoing income. In March, we completed a review of this asset class. The review included an assessment of current bond allocations and the wider Approved Product List (APL). We remain comfortable with the fixed income funds in your portfolio.

We believe the best way to allocate to global bonds is to diversify across different types of fixed income strategies, each with distinct risk/return profiles. In your portfolio we combine short-duration, high-quality credit, and government bonds. By blending these strategies, using low-cost core bond exposures alongside more active satellite funds, your global fixed income allocations have achieved better returns than standard bond indices, with less volatility. This strategy outperformed a global bond index across all measured periods over the last five years, including 2022 when considerable value came from short-duration strategies. Diversifying across bond sub-sectors and managers can enhance both the defensive and return aspects of a fixed income allocation. Each plays a specific role, which we outline below.

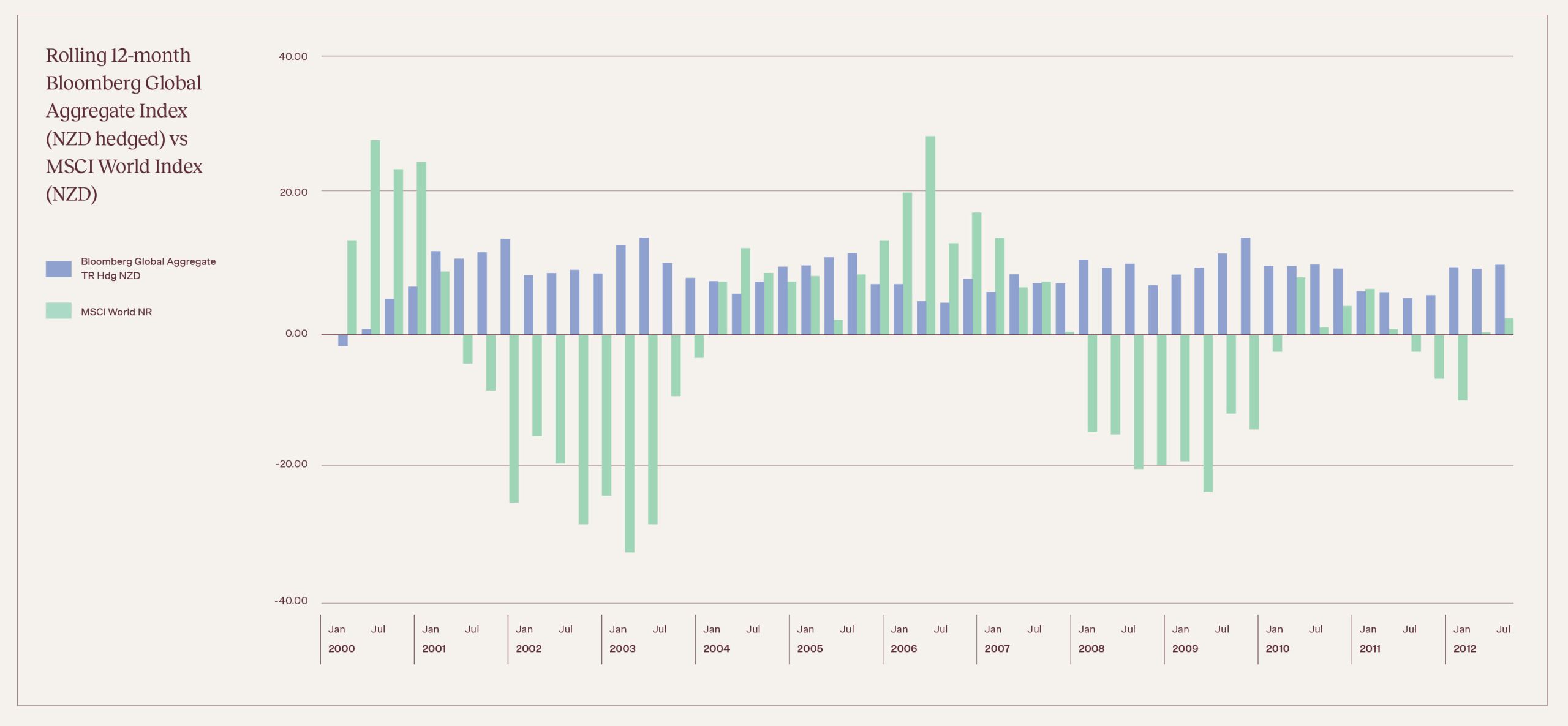

Government and Corporate Bonds (Core Duration): The safe haven. Sovereign bonds are seen as the ultimate safe haven and, for core bond exposure, are used alongside government-related entities and high-quality corporate bonds. They provide reliable income and a hedge during typical recessions. Figure 1 presents the long-term rolling annual returns of the Bloomberg Global Aggregate Index, which serves as the benchmark for global government and corporate bonds, covering the period since 1999.

Government bonds tend to perform best during periods of volatility, as central banks often cut interest rates in such times. This is illustrated in the chart on the following page, which shows the returns of global government and corporate bonds (blue line) versus global shares (green line) from January 1999 to December 2012. Bonds added considerable value to a portfolio during 2000–2003, when markets were down significantly because of the 2000 Technology, Media and Telecommunications (TMT) Bubble and the 2008 Global Financial Crisis (GFC), returning above 10% (NZD hedged) during both periods.

Core global bond returns faced notable headwinds in 2022, driven by rising interest rates and declining equity markets. Unlike during the TMT Bubble and the Global Financial Crisis, diversification benefits were limited. However, today’s environment of elevated global rates provides greater resilience against potential market downturns, as central banks now have significantly more flexibility to lower rates compared to 2022.

Short-Duration, High-Quality Credit: The stabiliser. These are bond funds that focus on short-term, high-quality corporate issuers. Their main function is capital preservation while providing a consistent yield above term deposits, with minimal sensitivity to interest rate moves. Here we have used short-duration specialist firms eg. Daintree. These funds have been among the best-performing segment of the fixed interest portfolio.

They held up significantly better than long-duration bonds during 2022’s rate spike and, because they are short duration, were able to rotate quickly into bonds offering higher coupons (interest rates), rebounding once conditions stabilised.